Watchlist: Loop Industries (LOOP)

$78M microcap, multiple deals, 46% insider ownership, rising institutional interest.

In my Watchlist series, I share new stocks I’ve recently added for investment consideration.The stocks mentioned in this series fulfill most or all of my investment criteria.

In a nutshell, I focus on small/mid-cap companies with improving fundamentals, but depressing valuations.

These are the kind of setups that helped me outperform the markets:

Today, I’ll be covering Loop Industries (LOOP).

By the end of this article, you’ll learn about:

The Company

The Fundamentals

The Valuation

The Risks

The Thesis

Disclosure: As of this article’s publication, I do not hold a position in the stock mentioned. This article reflects my initial research and analysis, which may or may not lead to an investment. Paid subscribers will be notified if I initiate a position.

Company

Ticker: LOOP

CEO: Daniel Solomita (founder)

Founded: 2014

IPO: 2015

Market Cap: $78M

Price: $1.61

52-Week Range: $0.85 - $2.29

All-Time Highs: $19.00 (January 2018)

LOOP is a clean technology company specializing in the advanced recycling of PET (polyethylene terephthalate) plastic and polyester fiber wastes.

The company aims to “accelerate the world’s shift toward sustainable PET plastic and polyester fiber and away from our dependence on fossil fuels”, alleviating the global plastic waste problem:

Since the 1950s, 8.3B tonnes of plastics have been produced.

~585B plastic drinking bottles are sold annually.

~25M tonnes of plastic textiles are landfilled or incinerated annually.

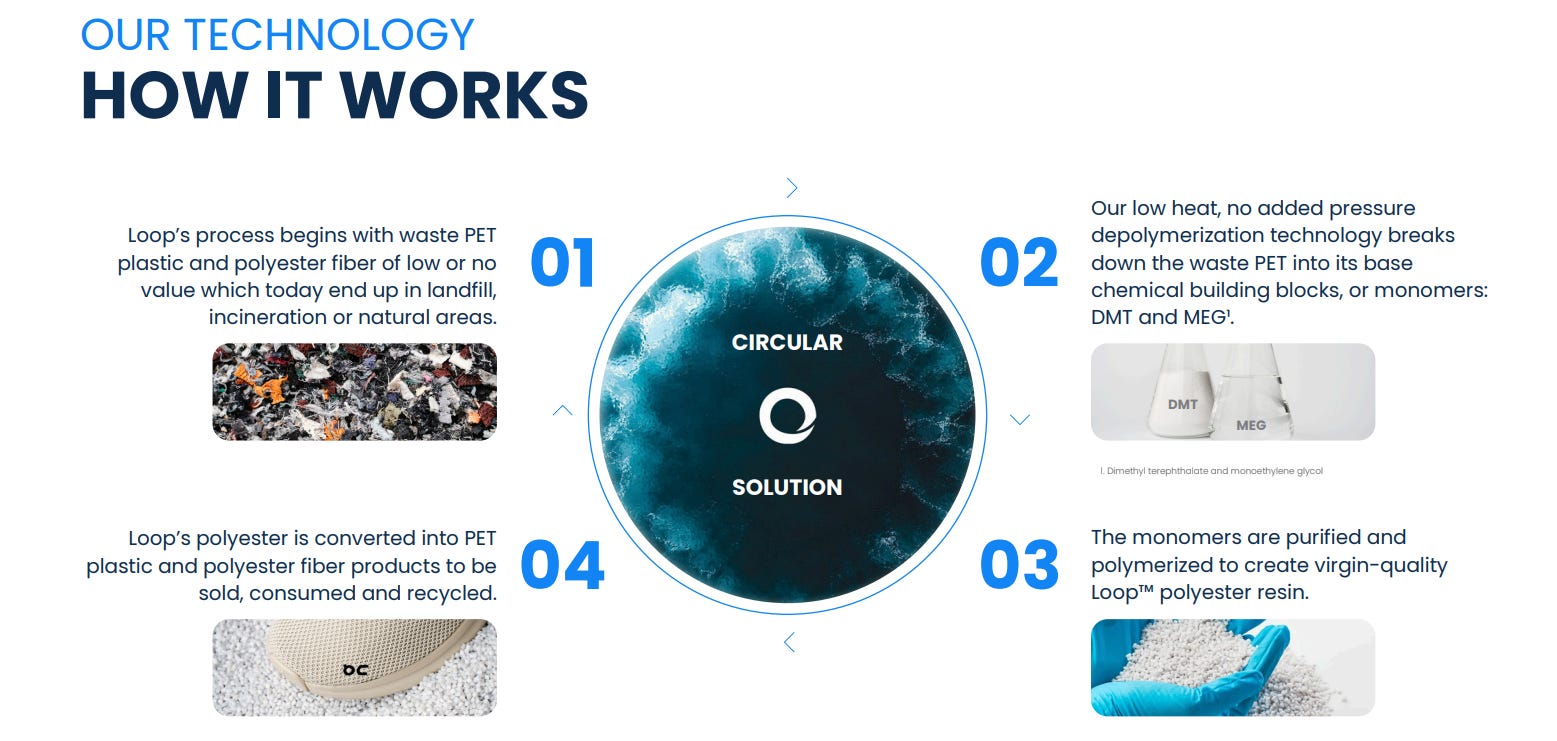

Through a chemical reaction called depolymerization, LOOP can turn wastes such as plastic bottles, food containers, and polyester activewear into its base building block monomers, DMT (dimethyl terephthalate) and MEG (monoethylene glycol).

The monomers are then separated, purified, and repolymerized into virgin-grade Loop™ PET resin, which some of LOOP’s customers can use to produce food-grade plastic packaging and polyester fiber.

LOOP’s technology has a few advantages over traditional mechanical recycling:

LOOP can recycle a wide range of PET plastic and polyester wastes, even those that contain impurities like labels, dyes, and other residues (these are called no or low-value waste). On the other hand, mechanical methods require labor-intensive processes such as sorting, washing, and separating, before the PET waste can be recycled. For instance, mechanical recycling cannot handle polyester blends containing other fibers like cotton and spandex, which is why they eventually end up in the landfill or incineration plant.

LOOP produces high-purity, virgin-quality, 100% recycled PET resin, which can be recycled infinitely with no quality degradation across cycles, thus supporting a circular economy. In contrast, mechanical processes like shredding, washing, and melting reduce the quality of the recycled PET, and after a few cycles, the quality of the material becomes too poor for further processing or reuse.

LOOP’s recycling process uses chemical reactions at low temperatures and no added pressure. This means lower energy usage, processing cost, and greenhouse gas emissions relative to mechanical processes, which often require high temperatures and pressure to melt and separate the waste. This also allows LOOP to recycle PET wastes with fewer equipment, steps, and labor, thus giving LOOP a cost advantage over traditional facilities.

Because of these three advantages, companies with ambitious sustainability goals are beginning to take notice of LOOP’s technology.

LOOP targets customers in the textile (fashion, home products, and automotive) and packaging (food and beverage, cosmetics, and pharmaceutical) markets.

This includes global brands like On Holding, Evian, and Garnier.

This is a testament to its technology and potential for future collaborations.

Fundamentals

Growth

While LOOP’s technology looks promising, the company has yet to generate meaningful, stable Revenue.

That’s because over the last five years, LOOP has mainly operated a small-scale production facility in Terrebonne, Canada, for testing purposes and finalizing its technology.

The company did earn Revenue through small projects, but it was still not enough to cover the day-to-day expenses of the company.

However, LOOP has recently signed several agreements with multiple partners, which have provided the company with sufficient capital to scale production.

On that note, LOOP plans to commercialize its technology in two ways: direct investments and licensing.

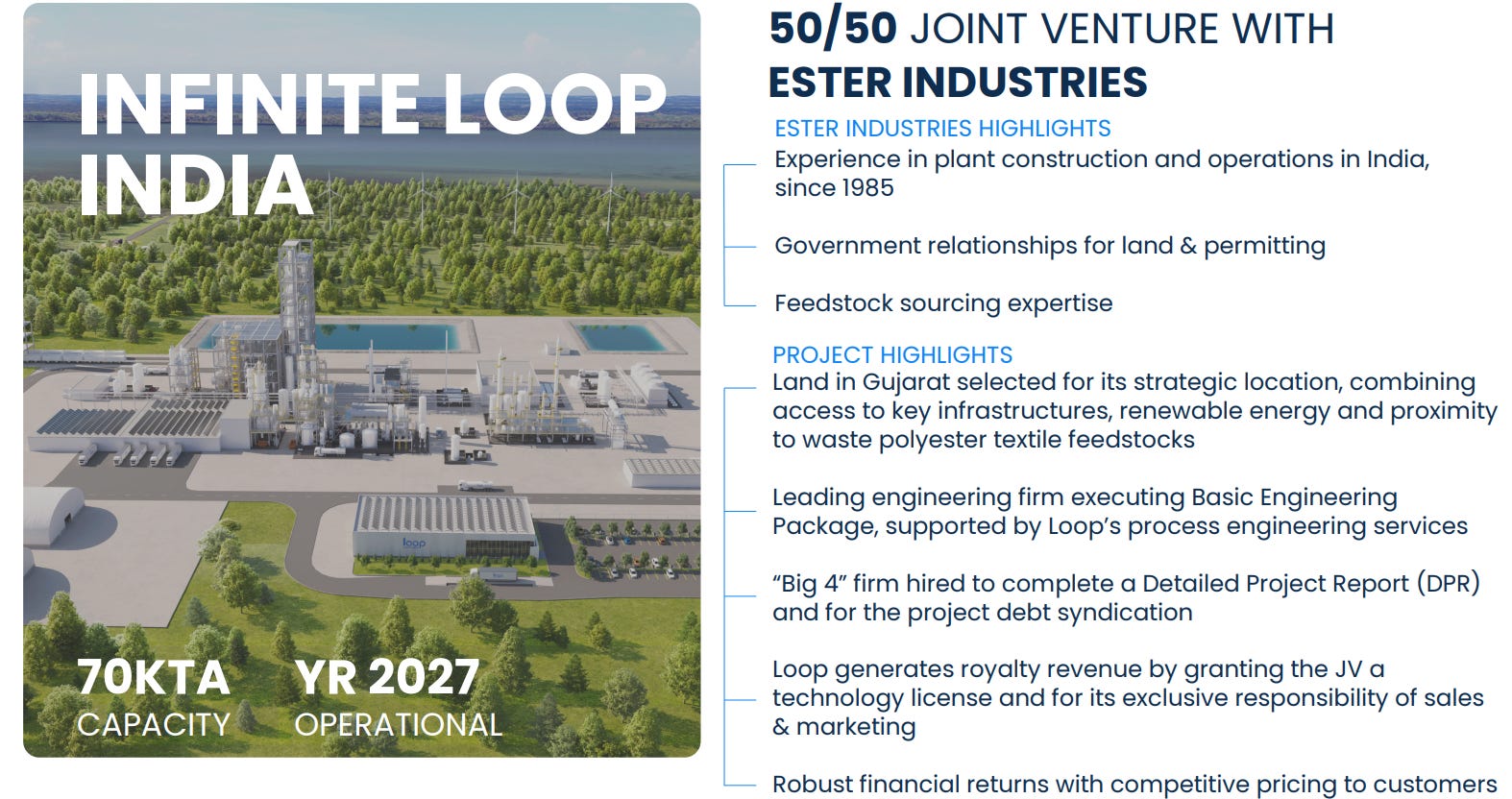

For instance, in May 2024, LOOP and Ester Industries (one of India’s key manufacturers of polyester films and specialty polymers) formed a 50/50 joint venture to build and operate a LOOP facility in India, and meet the growing demand for textile-to-textile polyester fiber.

It’s important to note that LOOP and Ester have had a 5-year working relationship, so the extension of their partnership is a confirmation of LOOP’s breakthrough technology.

A few months later (December 2024), LOOP also sold its first technology license to Reed Management SAS (owned by Societe Generale Group, a €40B+ market cap company), for one LOOP facility to be built in Europe.

As part of this agreement, LOOP gets 10% ownership of the facility (LOOP has the right to increase its stake to a maximum of 50%) and an upfront payment of €20M, consisting of €10M convertible preferred security and €10M of royalty fee.

Importantly, this licensing deal highlights the commercial readiness of LOOP’s technology.

In terms of the timeline, the India facility should be operational by 2027, while the European facility is expected to be operational by 2030 — yes, still a very long way to go.

With that said, management expects three key Revenue streams:

Profits from its commercial facilities.

Royalties via licensing its technology.

Exclusive engineering, sales, and marketing services for partners.

Below, you can see LOOP’s Revenue over the last couple of years.

Notice the big spike in Revenue in the quarter ended February 2025. This was mainly due to the €10M upfront royalty payment from Reed. LOOP also received $368K in engineering fees and $126K from the sales of PET resin from the Terrebonne facility.

While Revenue dropped significantly in the following quarter (ended May 2025), Revenue increased significantly YoY, mainly due to $244K in engineering fees.

Note that Revenue from the quarter ended August 2025 (Q2 FY2026) is not shown in the chart. For some reason, Fiscal.ai has not updated the data yet — they won’t need to as LOOP produced zero Revenue in the latest quarter.

However, in the next few quarters, LOOP should generate some Revenue as the company just executed a $1.5M engineering services agreement with ELITe to provide support for the development of the LOOP facility in India. Per management, this Revenue will start in November.

Notably, management anticipates entering into additional engineering service agreements like this, so expect a gradual ramp in Revenue over the next few quarters.

Moreover, LOOP has signed additional agreements with other players:

In September 2025, LOOP executed a multi-year offtake agreement with a leading sportswear brand for the sale of its branded textile-to-textile Twist™ polyester. Per management, this sports brand is an existing customer of its Terrebonne facility. With that, I believe this customer is On Holding, the Swiss-based premium sportswear brand, which already has a partnership with LOOP related to the Cloudeasy Cyclon shoe. Nevertheless, management highlighted that this is “a very strong contract, very bankable contract”.

In September 2025, LOOP also executed an offtake agreement with Taro Plast, an Italy-based specialty polymer manufacturer. Under this agreement, LOOP will supply Loop™ DMT to Taro Plast.

In September 2025, LOOP formed a strategic alliance with Hyosung TNC, a leading player in the South Korean polyester yarn market and the world’s largest manufacturer of spandex. Under this collaboration, LOOP will supply Twist™ polyester to Hyosung TNC.

In August 2025, LOOP formed a strategic alliance with Shinkong, a leader in Taiwan’s polyester industry and a top-tier supplier of high-performance textiles for apparel brands. Under this collaboration, LOOP will supply Twist™ polyester to Shinkong.

Excitingly, management highlighted that they “continue to advance negotiations with additional apparel and CPG brands to secure further offtake agreements” and that they “anticipate having other supply agreements finalized by the end of the year”.

That said, the recent influx of deals should generate meaningful Revenue once the India and Europe facilities go live, thus serving as positive catalysts for LOOP stock.

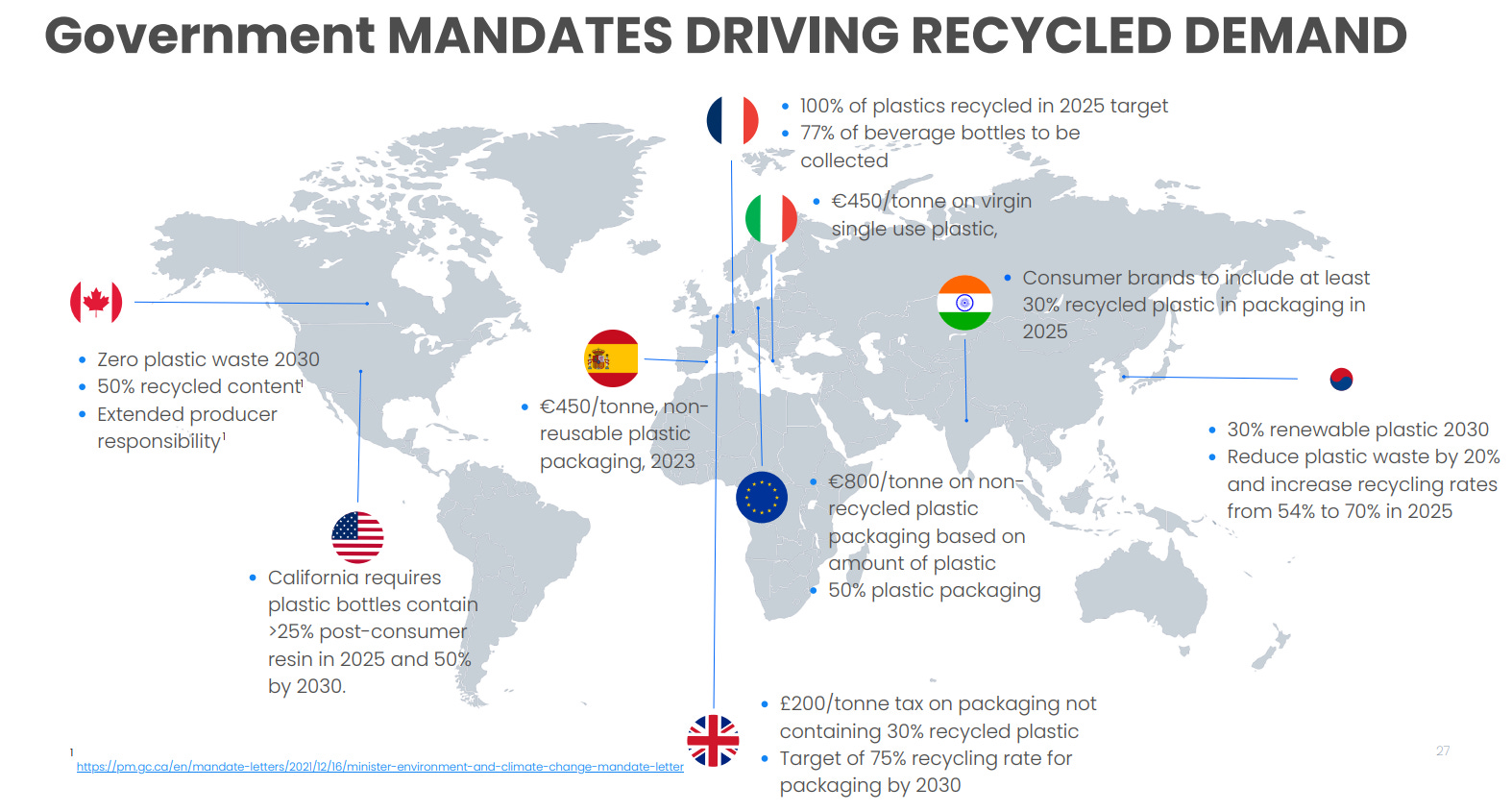

Whatever it is, rising consumer awareness of plastic pollution and climate change, as well as the increasing commitments of brands and governments worldwide to make the transition to a circular plastic economy, should serve as major tailwinds for clean technology companies like LOOP.

Profitability

In its most recent quarter, Net Income is still negative at $(3.2)M in the quarter ended August 2025 (again, not shown in the chart below).

Net Income did turn positive briefly in Q4 FY2023 and Q4 FY2025, due to an asset sale and the €10M upfront royalty payment from Reed, respectively, but aside from that, Net Income has largely been in the red.

This is no surprise given that LOOP has yet to commercialize its technology.

However, as LOOP’s deal pipeline grows and as its facilities begin production, we can expect Net Income to flip positive due to operating leverage.

But again, it will take time — 2 years at the very least.

Until then, LOOP depends heavily on the capital markets and strategic partners to provide the funds it needs to build factories, pay salaries, and expand production.

Health

As of Q2, the company holds $9.9M in Cash, which should be good to fund operations for another three to four quarters. For context, Q2 Cash Operating Expenses were $2.4M, representing an annual run rate of approximately $9.2M.

In the meantime, management is looking for ways to secure additional capital for the India JV and for operating expenses until the start of the India facility in 2027, so expect some equity and debt raises along the way. After all, the total estimated capital cost for the India JV project is $176M, and since it’s a 50/50 JV, LOOP is responsible for approximately $88M in contributions.

Encouragingly, despite being in the pre-commercialization stage, the deal pipeline seems to be ramping up — additional offtake agreements, licensing fees, and engineering services should generate some level of Free Cash Flow to help finance future projects.

More importantly, this should reduce the need for upsized external capital, limiting unnecessary shareholder dilution and balance sheet pressure.

Valuation

Given its unpredictable sales and cash flow, valuing LOOP stock seems like an impossible task.

But we can look at what analysts, institutions, and insiders are doing to gauge the overall sentiment on the stock.

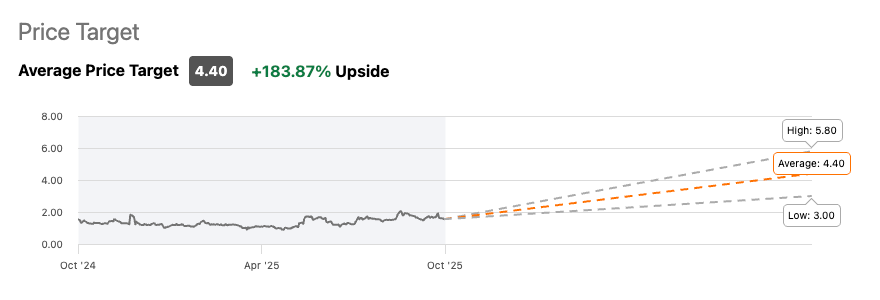

For one, analysts are bullish on the stock with an average price target of $4.40, representing an upside potential of 184%.

There’s one caveat. Analyst coverage is very limited, with only 4 analysts covering the stock and 2 analysts issuing a specific price target. As such, take this price target with a grain of salt.

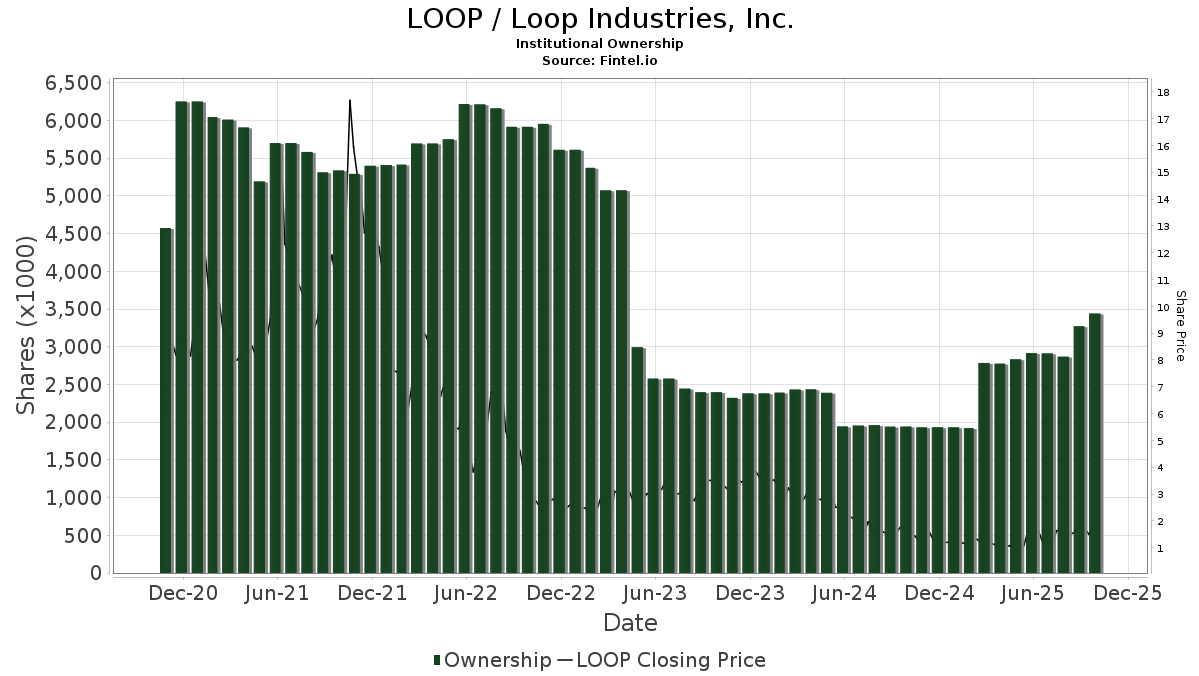

On the other side, institutions are beginning to increase their stakes in LOOP stock. As you can see below, institutions were dumping shares of LOOP as its share price collapsed from $17 to $1.

However, institutional ownership has been increasing over the last few months, likely driven by the company’s robust deal momentum recently. This is a signal of renewed institutional confidence.

Also, something worth pointing out is that the €10M convertible preferred security issued by Reed has a 5-year term and a conversion price of $4.75 per share. The deal was closed on 12 December 2024, which, at that time, LOOP was trading at $1.23.

In other words, Reed is confident that LOOP’s share price will be higher than $4.75 within 5 years, which is nearly a 300% increase from the deal date. As of this writing, LOOP is trading at $1.61, implying a 200% upside to $4.75.

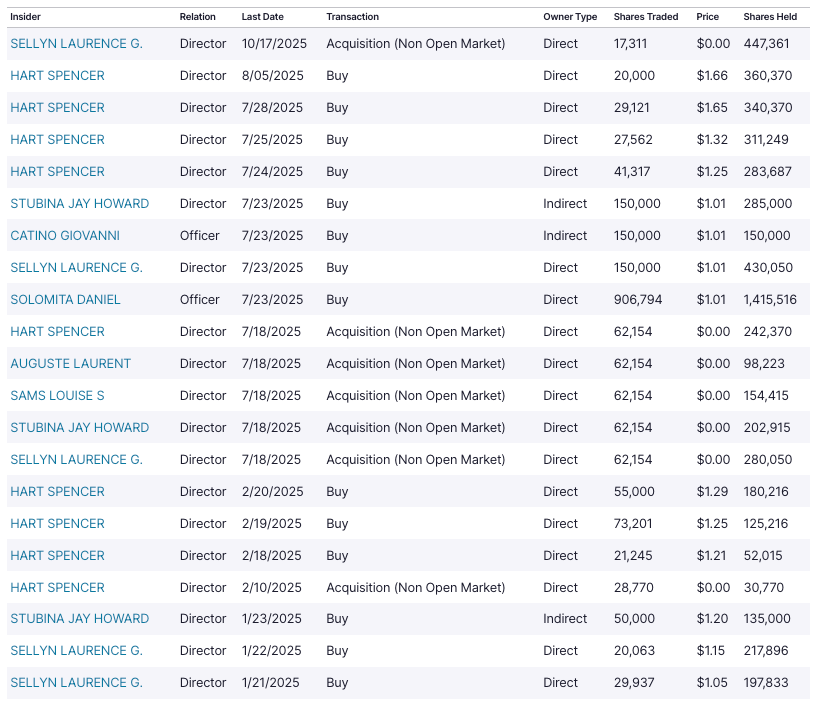

Finally, insiders have been buying the company’s stock aggressively. According to Nasdaq, insiders bought shares in the open market 14 times this year.

There have been no sales so far this year.

Most notably, insiders own nearly half of the company, with CEO Daniel Solomita having a 42% stake in the company.

I checked the company’s first DEF 14A proxy statement (2018) and saw that the CEO held 19.6M shares.

Today, he holds 20.0M shares, relatively unchanged from 7 years ago.

That’s unwavering commitment.

That’s shareholder alignment.

That’s a whole lot of skin in the game.

While it may be difficult to find a fair value estimate on LOOP stock, we can agree that analysts, institutions, and insiders are all bullish on the stock.

Risks

Financing: LOOP must obtain substantial funding to support its equity contribution in the India JV and to cover operating expenses until the facility becomes operational. Insufficient funding could delay or stop the project, hindering LOOP’s growth ambitions. Moreover, LOOP may be forced to raise external capital under unfavorable terms, including high dilution or asset-backed debt raises.

Deal Termination: LOOP’s success hinges on securing offtake agreements with major global apparel and CPG brands — these agreements guarantee a Revenue stream for LOOP. In addition, LOOP relies on strategic partners like Ester and Reed to scale its technology. While it’s encouraging to see this deal momentum, realize that these deals are not set in stone. Deal terminations, which have happened before, jeopardize LOOP’s commercialization plans, and the stock could sell off as a result.

Business Model Viability: LOOP is still in its pre-commercialization stage, and therefore, is still unprofitable and cash-burning — no one knows when LOOP will turn a profit. Additionally, the long-term financial profile of the business, including cost structure and profit margins, remains uncertain.

Thesis

Look. LOOP is an incredibly risky bet.

The company has yet to commercialize its technology. It’s still unprofitable. It still needs to raise capital in the near term, which may lead to shareholder dilution. Then, there’s the potential for deals to be terminated, and even if they proceed, the timeline remains uncertain. Above all, we don’t know for sure if LOOP has a viable business model that can deliver attractive returns in the long run.

Perhaps that is why the stock trades where it is today: down 90%+ from its all-time highs, at a Market Cap of just $78M.

I typically invest in high-growth, cash-flow-generative companies trading at a $1B to $10B Market Cap, so the million-dollar question is: Why am I considering LOOP?

For one, I want to support clean technology companies that make the world a better place.

Plastic pollution is a serious problem. Some of you who live in developed regions like the US or Europe may not see it, but in less developed countries like Indonesia (where I live), they’re plagued with plastic waste. Land, sea, and even the air (plastics are often incinerated), they’re everywhere, and it’s very discouraging to see.

By investing in LOOP, I hope to follow the company’s journey in advancing a circular plastic economy.

The second reason why I’m considering investing in LOOP — for more selfish reasons — is, of course, to make money.

As I see it, LOOP stock looks undervalued for its massive potential. And despite significant business progress over the last few quarters, the stock is still down 90% from its peak, giving investors ample margin of safety.

Furthermore, partners, brands, insiders, analysts, and institutions are more confident than ever in LOOP, potentially signalling an inflection point for the company.

Yes, it may take a couple more years before LOOP enters commercialization, but if I waited till all systems go, it would already be too late.

By being early (and patient), I can capture more upside.

But there’s a big but: LOOP stock could go nowhere for the next few years. Heck, it could even go to zero.

This is why risk management is very important.

If I were to initiate a position in LOOP, it would be a fraction of my portfolio — 2% max.

All in all, LOOP is a high-risk, high-reward play.

While this company is beyond my typical coverage, I thought I’d venture outside my comfort zone and look for opportunities where I normally wouldn’t.

At the same time, I thought it’d be an interesting stock idea to share with you guys.

That said, thank you for reading, and I hope you have an amazing day!

Disclaimer: This article is intended for informational, educational, and entertainment purposes only. Content presented by Riyado Sofian reflects his personal research and opinions, and does not constitute, and should not be construed as, investment advice.

This is a great analysis. Well done

Yes, similar to private equity investing. The product seems to be so disruptive, it has to work. Its worth buying a few shares, just to be part of the story.